Date/Time: May 12, 2026, 9:00 AM – 10:00 AM

Attendees: CEO Jung Woo-jin, CFO Ahn Hyun-sik, NHN Cloud CEO Kim Dong-hoon

Agenda: NHN Q1 2026 Earnings and Future Strategy

■ Summary of NHN Q1 2026 Earnings and Status

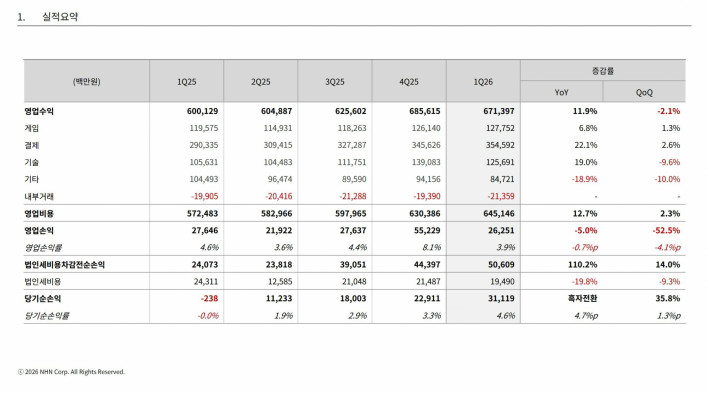

- Revenue: ₩671.3 billion (+11.9% YoY, -2.1% QoQ)

- Operating Profit: ₩26.2 billion (-5% YoY, -52.5% QoQ)

- Net Income: ₩31.1 billion (Turned to profit, +35.8% QoQ)

■ Revenue by Business Division

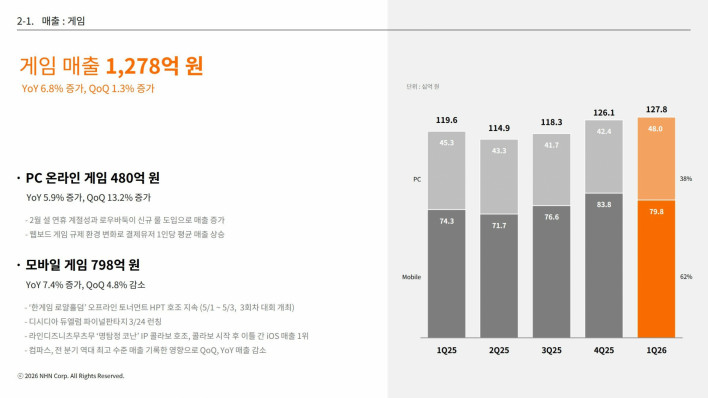

- Games: ₩127.8 billion (+6.8% YoY, +1.3% QoQ)

ㄴ Average revenue per user (ARPU) increased due to changes in the regulatory environment for web-board games

ㄴ Successful market entry and stable traffic for Dissidia Final Fantasy: Duelium

ㄴ LINE: Disney Tsum Tsum's 'Detective Conan' IP collaboration performs well, reaching No. 1 in iOS revenue two days after launch

ㄴ #Compass records all-time high quarterly revenue, driven by 'Chainsaw Man' collaboration

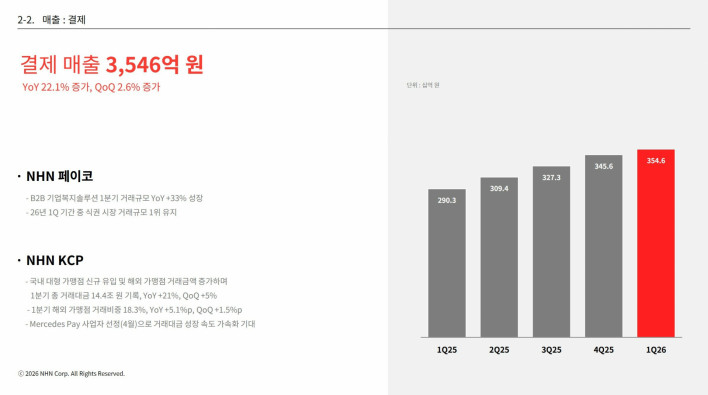

- Payment: ₩354.6 billion (+22.1% YoY, +2.6% QoQ)

ㄴ Maintained #1 position in the meal voucher market in Q1 2026; total transaction volume reached ₩14.4 trillion, driven by growth in domestic large-scale merchants, new user acquisition, and overseas transaction volume

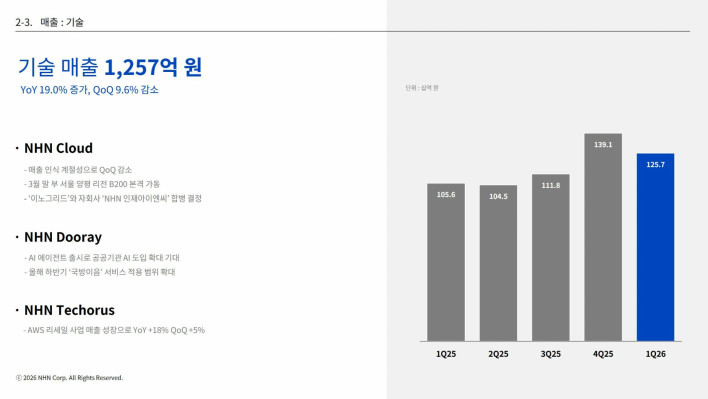

- Technology: ₩125.7 billion (+19% YoY, -9.6% QoQ)

ㄴ QoQ decline due to seasonality in NHN Cloud revenue recognition; decision made to merge subsidiary 'NHN Injae INC' into 'AnoGrid'; expansion of 'Gukbang-Eum' service coverage planned for H2

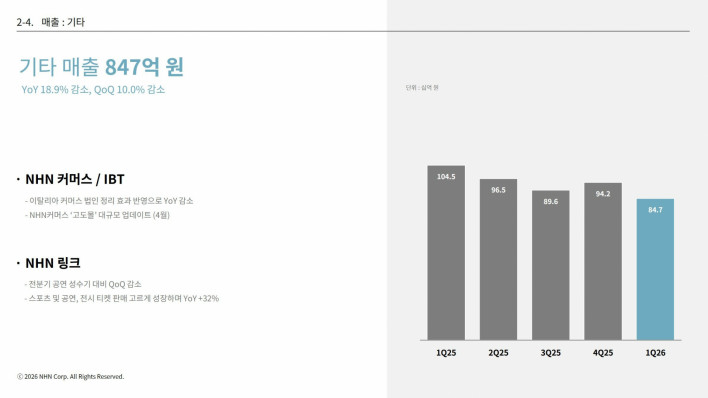

- Other: ₩84.7 billion (-18.9% YoY, -10% QoQ)

ㄴ YoY decline due to the liquidation of the Italian e-commerce entity; QoQ decline compared to the peak performance season for live events in the previous quarter

■ Cost and Profit Structure

- Operating Expenses: ₩645.1 billion (+12.7% YoY, +2.3% QoQ)

- Payment Commissions (+0.4% QoQ): Increase in revenue-linked commissions due to NHN KCP revenue growth

- Labor Costs (+7.5% QoQ): Wage increases at NHN and consolidated subsidiaries, and inclusion of fixed bonuses at NHN KCP

- Advertising expenses down 1.5% QoQ: Decrease in marketing spend for '#Compass'

- Depreciation (+21.9% QoQ): Recognition of amortization for right-of-use assets and tangible assets related to NHN Cloud's government AI projects

- Operating Profit: ₩26.2 billion (-5% YoY, -52.5% QoQ)

- Net Income: ₩31.1 billion (Turned to profit YoY, +35.8% QoQ)

- Reflects gains from the disposal of financial assets measured at fair value through profit or loss by a subsidiary

■ Q&A

Q. Could you discuss the game division's strategy for this year and any additional new titles? I am also curious about the revenue guidance for the Yangpyeong data center and whether the amortization of right-of-use assets seen in Q1 will continue into Q2.

CEO Jung Woo-jin = Regarding the game business, we are targeting the Japanese market. We are currently preparing or in the process of securing contracts with IPs that have high brand recognition in Japan.

NHN Cloud CEO Kim Dong-hoon = As mentioned in our previous earnings call, we are targeting ₩300 billion in revenue over five years for the Yangpyeong project, and there is no change to that plan. While there is potential for revenue upside due to the recent surge in GPU demand, it is difficult to reflect this in our guidance at this time.

Q. I would like to confirm the guidance for advertising expenses relative to revenue this year. Also, for the cloud business, which generated ₩220 billion in revenue and roughly ₩20 billion in losses last year, what level of revenue can we expect this year.

CFO Ahn Hyun-sik = Last year, we spent ₩86 billion on advertising. With a relatively high number of new game launches this year, we expect expenses to increase by around 10% compared to last year. While it is difficult to provide definitive guidance due to many variables, we are currently projecting 30% growth for the Yangpyeong project.

Sort by:

Comments :0